Why repeated inflation shocks reshape what people believe, and what that does to markets.

Last Thursday, the latest PCE inflation report landed, and depending on which headline you read, you came away with two very different impressions. The market-friendly version focused on the parts that came in a touch softer than feared. The less comforting version focused on the fact that the core measure is still running well above the two percent target, and has been for years now. Both readings miss the more important point, which is what successive years of inflation prints like this one quietly do to the way ordinary people think about prices going forward. That shift in belief, more than any single data release, is what shapes the next few years of markets.

How Repeated Shocks Change Behavior

When prices spike once, most people treat it as a one-off. They grumble about gas or eggs, wait for things to settle, and carry on. When prices keep climbing for several years in a row, even at a slower pace, something different happens. People stop treating each new shock as temporary and start adjusting their behavior in advance. A worker who has watched her grocery bill climb every year for five years stops believing the next year will be different, and asks for a bigger raise. A small business owner who has absorbed cost increases on materials, insurance, and labor stops absorbing them and starts passing them through.

None of those individual decisions seem like much, but taken together, across an entire economy, they are how a temporary inflation problem becomes a permanent one. The original shock fades, but the behavior it produced does not, and the behavior itself is what keeps prices climbing.

Economists call this the un-anchoring of inflation expectations. After enough years of watching prices rise faster than they used to, the assumption that things will eventually settle back to normal disappears, replaced by an assumption that costs just keep going up. Once that sets in, it is extremely hard to dislodge because everyone is acting on it at once.

The last time this happened in the United States was the 1970s, and it took Paul Volcker raising rates into the high teens and triggering a deep recession in the early 1980s to fix. Every central banker since has been trained on that lesson, which is why the Fed will not declare victory until long-term expectations come back down.

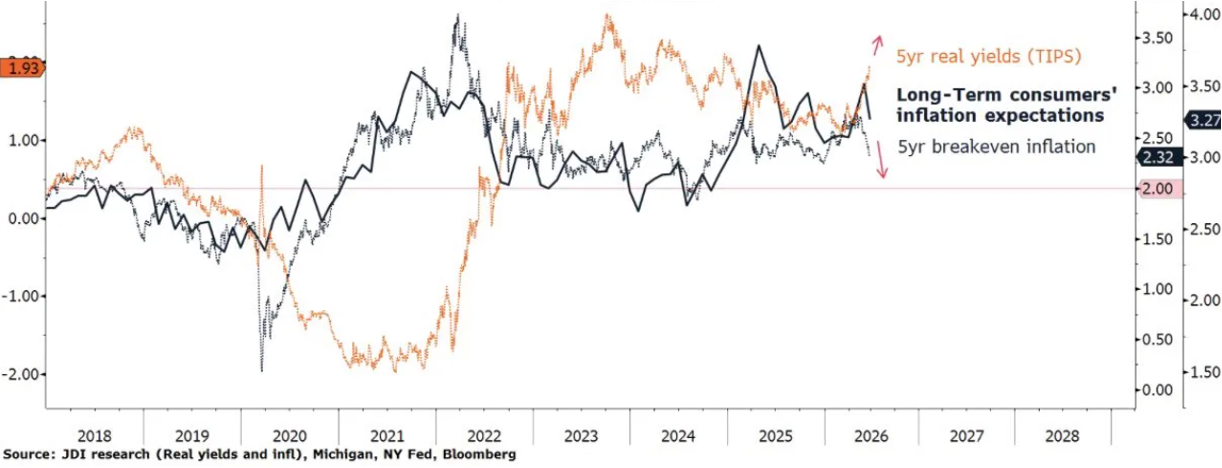

What Households Are Signaling

The way to measure this is to look at what households say they expect inflation to do over the long run. Surveys from the University of Michigan and the New York Fed have asked that question for decades, and the answers right now are uncomfortable. Long-term inflation expectations have drifted higher than they have been in a generation, and they are not coming down even as the most-watched inflation prints have eased. That gap is the most important signal in markets right now, and it is one almost no one is talking about.

Where Households and Markets Disagree

Why this matters: The dark line is what households expect inflation to do over the long run, and it has climbed near the highest levels of the past several years. The dotted blue line is what bond markets are currently pricing, which has eased back toward two percent. Investors have been celebrating the dotted line and ignoring the dark one. The dark line is the signal the Fed is trying to pull lower.

There is also a political layer worth noting. The Fed is meant to be independent of politics, but it usually faces some pressure to ease policy in an election year, and this is a midterm year. That pressure has been unusually quiet because voters punish high prices more than high rates. As long as households remain focused on the cost of living, the political incentive to push for premature cuts is weaker than usual, which gives the Fed more room to stay restrictive just as the data is telling them they need it.

Why This Rewrites the Investment Playbook

For four decades, the dominant story was the slow grind lower in interest rates and the slow grind higher in asset prices. Each inflation scare turned out to be temporary and expectations stayed anchored. The playbook investors built around that environment, owning long-duration growth stocks, long-dated bonds, and asset-light businesses, was the right one for the world it was designed for.

That world is shifting. When repeated shocks start to change what people expect, the playbook has to change with it. The companies that thrive in a stickier-inflation environment are not the same ones that thrived in a falling-rate one. Recognizing the shift early is the difference between adapting and getting caught.

What This Means for a Portfolio

This is not a moment to abandon AI or growth investing. The underlying demand is real and the physical buildout is happening regardless of what inflation does next. What is likely to change in the second half of 2026 is which kinds of companies inside the broader market get rewarded. The investors most likely to do well from here tend to do a few specific things:

• Rotate within the AI theme rather than out of it. Move from the most speculative, balance-sheet-dependent names toward the businesses with real assets, contracted cash flows, and proven access to capital, including the power, transmission, and data center operators that own the physical layer of the buildout.

• Trim the longest-duration, most rate-sensitive equity exposure. Companies whose value lives almost entirely in distant future earnings are the most exposed to real yields staying high.

• Add real-asset exposure as a hedge. Energy producers, materials, and infrastructure all benefit when paper claims lose ground to physical things, which is the path stickier inflation tends to put us on.

• Lean toward businesses that keep their pricing power. Healthcare, biotech, certain consumer staples, and other companies that can quietly raise prices without losing customers are the ones whose earnings actually keep pace with a stickier inflation backdrop.

The Bigger Picture

The Thursday PCE release will be quickly forgotten, but what will not be forgotten, by the households and businesses living through it, is the cumulative experience of several years of prices rising faster than they used to. That experience is reshaping behavior in ways that take a long time to reverse, and it is the underlying reason this cycle does not look like the last one. The investors who recognize that early, and adjust how their portfolio is built to match, are the ones most likely to come out ahead.