Why a three-hundred-year-old story is worth keeping in mind today.

In the early 1700s, a Scottish economist named John Law convinced the French government to let him run an experiment. France was buried under debt from years of war, and Law proposed something radical for the time: replace the country’s gold-backed currency with paper money, expand the supply consistently to help pay government debts, and pair it with a state-sponsored joint stock company that would attract investment from across Europe.

The company was called the Mississippi Company, and the experiment worked spectacularly well, for a while. Law printed money, the supply of credit expanded, the Mississippi Company’s share price soared, and Paris became the financial capital of the world almost overnight. Fortunes were made in months. The word “millionaire” was coined to describe the speculators who got rich on Mississippi shares.

Law himself became, briefly, one of the wealthiest people in Europe, but the most important part of the story is that he used his paper fortune to buy real assets. Estates, country properties, real holdings across France. By the time the bubble he had engineered collapsed in 1720, the paper wealth of nearly everyone involved was wiped out. The shares were worthless. The currency was discredited, but the man who had run the entire scheme had quietly converted enough of his paper profits into land that he remained a substantial landowner even after the system he built fell apart.

The man who understood the mechanics of the bubble best, because he had designed it, still chose to convert paper wealth into physical wealth before the cycle turned. This distinction between financial assets and real assets has not gone away, and only one of them keeps its value when the currency deteriorates.

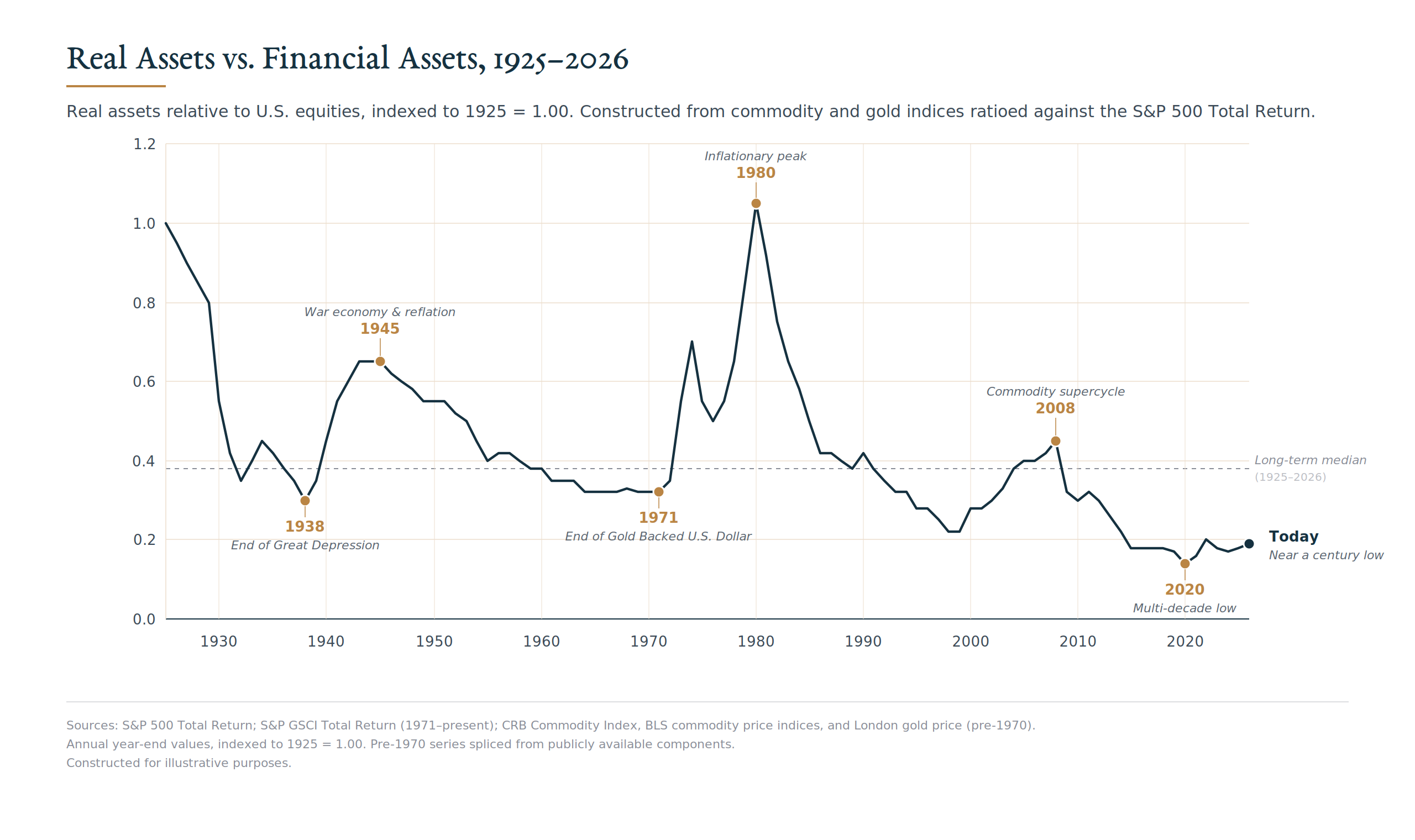

Why this matters: Real assets have been losing ground to financial assets for more than four decades. The ratio now sits near a century low, and the same conditions that drove that decline (falling rates, contained inflation, and credit expanding into financial markets rather than the real economy) are the ones now beginning to change.

What You Actually Own

Most investors do not stop to think about what their portfolio actually represents. When you own a stock, you own a claim on a company’s future cash flows, denominated in dollars. When you own a bond, you own a promise to be paid back, also in dollars. When you have money in the bank, you have a digital entry that says the bank owes you dollars. Every line on a typical brokerage statement is a claim on something else, denominated in the currency of the country issuing it.

Real wealth is different. Land does not pay you back in dollars. It just sits there and exists. The same is true of a building, a farm, a producing oil well, an ounce of gold, or a piece of industrial equipment. These things have value because they are useful, not because someone has promised to pay you for them.

In normal times, the distinction can feel abstract and academic. Claims and the actual stuff move roughly together, and most investors prefer the claims because they are easier to own and trade. Although when the currency itself starts to lose purchasing power faster than expected, the distinction starts hitting closer to home. The actual stuff holds its value, and the claims denominated in a weakening currency quietly lose ground.

Why Financial Assets Have Won for Forty Years

The story of the past forty years in financial markets is, in large part, the story of cheap credit. Interest rates fell almost continuously from the early 1980s through the early 2020s, and credit expanded faster than the underlying economy was growing. When credit grows faster than the real economy, it has to go somewhere. For most of this era, it flowed into financial assets rather than the real economy.

Several forces reinforced the trend:

- Falling rates. Lower rates mechanically raise the present value of every future dollar of earnings, which boosts financial valuations even when nothing else changes.

- Globalization. Cheaper imported goods kept measured inflation low, which let central banks keep money loose without obvious consequences.

- Technology. Asset-light businesses generated enormous profits on relatively little physical capital, which favored the kinds of companies that dominate equity indexes.

- U.S. dollar reserve status. The dollar’s role as the world’s reserve currency drew steady foreign capital into U.S. financial assets, supporting valuations through cycles that would have stressed other markets.

This is the era we have lived through. Financial wealth grew faster than the productive economy underneath it, and a generation of investors built portfolios, habits, and assumptions around it. It worked because the cheap credit stayed contained inside the financial system. It bid up stocks, bonds, and high-end assets, but it did not flow in meaningful volume into the prices of everyday goods and services.

That is the dynamic that is starting to change.

Why This Pattern May Be Turning

Government debt has reached levels that historically only happened in wartime, and the realistic path forward is not austerity or default but slowly inflating the value of the debt away by allowing the currency to lose purchasing power over time. That is what governments in this position almost always do.

At the same time, the financial wealth that accumulated for forty years is finally beginning to flow back into the real economy. Capital projects, second homes, AI infrastructure, defense build-outs, and the services provided to an increasingly wealthy class of asset owners all turn into spending on real-world goods and labor. That pushes up the prices of physical things.

None of this points to runaway inflation, but it points to inflation that settles at a higher resting level than the prior decade, with rates that do not fall as easily, for a long time.

What This Means for Your Portfolio

The pattern Law lived through is playing out again, at a slower speed. Paper wealth that looks fine on a statement can steadily lose purchasing power against the price of the actual stuff.

The investors most likely to navigate this well do a few specific things:

• Trim long-duration claims on dollars. The highest-multiple growth stocks and the longest-dated bonds are the most exposed to a rising-rate, sticky-inflation environment.

• Redirect capital toward real assets and the equities of companies that own or produce real things. Energy, materials, infrastructure, real estate with genuine pricing power, and agricultural land.

• Hold some allocation in monetary metals like gold. Not as a speculation, but as a hedge against the very dynamic this letter has been describing.

• Keep owning equities of high-quality businesses with pricing power. Those are themselves a partial claim on real assets, but trim the most rate-sensitive parts of the equity book.

What these investors do not do is abandon financial assets. They simply rebalance toward the real side of the ledger in a way most of their peers, anchored in the prior decade, are slow to consider.

The Bigger Picture

Three hundred years ago, John Law watched paper wealth multiply in ways the world had never seen, and quietly converted his into land. His instinct was that claims on a fragile currency are one kind of wealth, and the actual stuff is another, and over long enough horizons, only one of them keeps its value when the other loses it.

The forty-year stretch in which financial assets enormously outperformed real ones was a real opportunity. The investors who do equally well from here will likely be the ones who recognize that the wind is no longer blowing as strongly in the same direction.