Part three of a three-part series on the phases of the AI investment cycle.

The first two acts of this cycle have been about AI working inside the digital world. First looking at the current investment in infrastructure and the foundational models that run on top, then taking a contrarian view of how software could be the next wave of the AI build due to ownership of proprietary data and existing enterprise relationships.

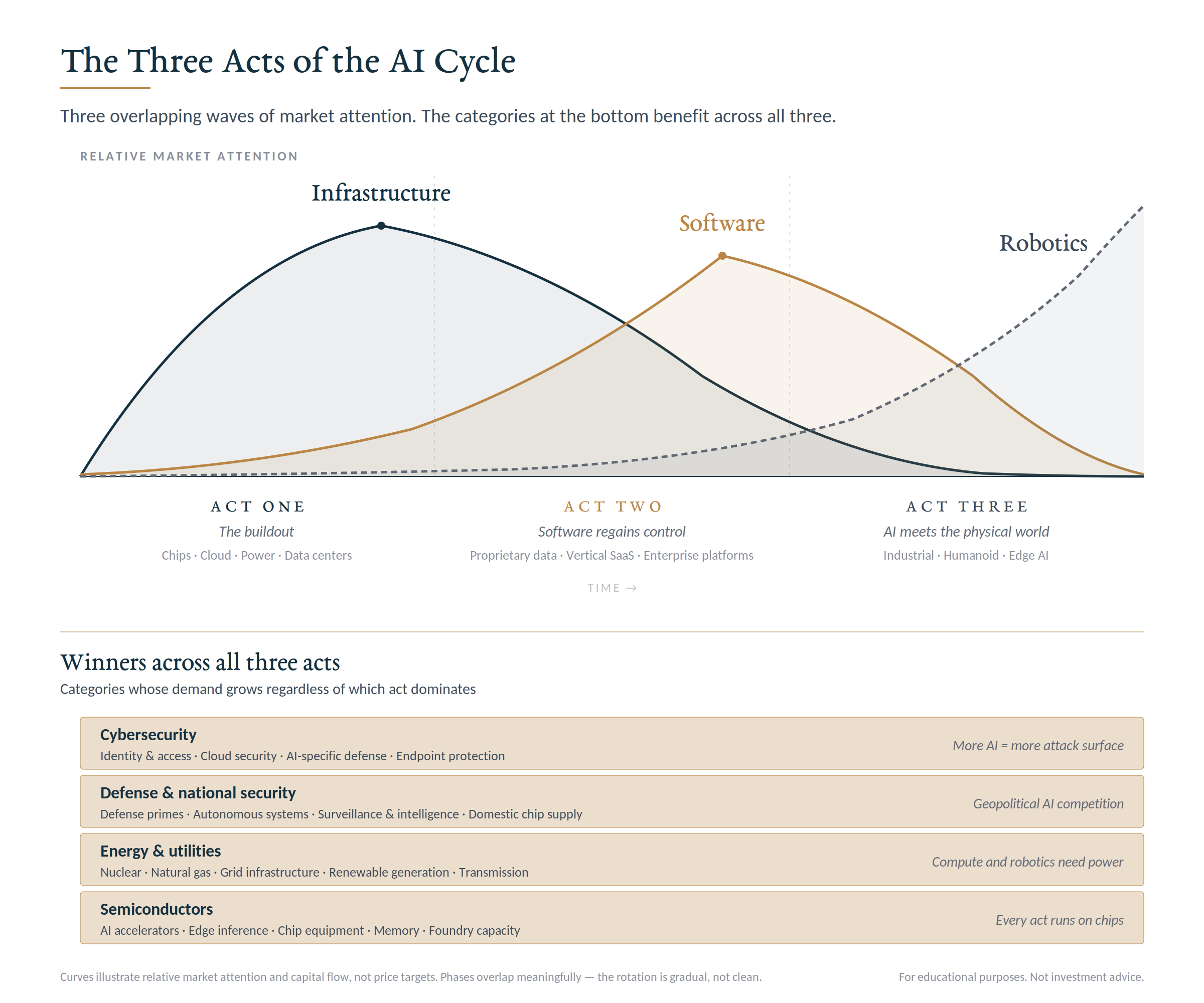

The third act is when AI leaves the screen.

This is the period when artificial intelligence merges with physical hardware and starts to operate in the real world through robotics, autonomous systems, sensors, and machines that can move and act on their own. It is the phase that will likely change daily life in ways the first two acts will not, and it is also the phase that is still the furthest from being a clean investment thesis.

Today I want to walk through why this matters now, even if the opportunity is 2-3 years from being an investable theme in the way the first two acts already are.

Why this matters: The third act has the longest runway and the most uncertain timing. Understanding the shape of it now is the first step before thinking about portfolio allocations.

What the Third Act Actually Is

The first two acts have changed how knowledge work gets done. Code, content, analysis, customer service, research, and back-office workflows are all being affected. The third act extends AI into the physical layer with the unifying idea that AI stops being a tool you interact with through a screen and starts being a presence that acts on the world directly. Given how much of our lives are currently spent looking at screens, I think this is one of the more difficult innovative transitions for us to imagine right now. The shift from screen-based AI to physical AI represents a different kind of relationship between humans and the technology that surrounds them.

Despite the significant innovations and investments within the first two acts, the third act has the largest potential economic impact. Knowledge work is roughly a third of global GDP. Physical labor, manufacturing, logistics, healthcare delivery, and transportation are a much larger share. Even modest improvements in physical productivity translate into enormous economic value.

Why This Phase Is Different From the First Two

The first act is a capital cycle focused on building the infrastructure, deploying the chips, and securing the power. The second act will be a software cycle, layering AI onto proprietary data, monetizing through existing customer relationships, and capturing value at the application layer.

The third act is a hardware cycle, and hardware behaves differently than either of the first two.

For one, hardware takes longer to develop. The companies leading this phase are building physical products that have to work reliably in unpredictable environments, comply with safety regulations, and survive real-world conditions, all of which extends every timeline by years.

Hardware also requires more capital than software, and the returns take longer to materialize. The companies investing in robotics, autonomous vehicles, and humanoid platforms today are spending billions of dollars on capability that will not generate meaningful revenue for several more years.

Finally, hardware faces real-world adoption friction that software does not. Customers have to retrain workforces, retrofit facilities, and absorb operational disruption. Even if the technology works, the deployment and adoption will take time.

What Will Likely Drive the Third Act

A few themes worth understanding:

- Sensors, vision systems, and edge AI hardware. The picks and shovels of the third act that is already showing early trends due to robot manufacturer investment.

- Humanoid and general-purpose robotics. The category attracting significant attention because the long-term implications are the largest.

- Autonomous vehicles and transportation. A decade of investment is starting to produce commercial deployments. Whether the economics work at scale is still an open question.

- Industrial and warehouse robotics. This is the most mature category. Although it has narrower applications, the revenue is growing.

- Drone and aerial systems. Both commercial and defense applications are expanding, often supported by direct government investment.

- Surgical, medical, and assistive robotics. Where the regulatory bar is highest but could produce the most profitable machines.

Why This Is Worth Understanding Now

The natural question is why an investor should pay attention to a phase that is 2-3 years from being a meaningful portfolio decision. A few principles worth holding onto:

- Most investors are not paying attention to it yet. The companies that will lead the third act are starting to take recognizable shape now (e.g., picks and shovels companies within robotic hardware). Start watching them now while expectations are still forming and they are not consensus.

- The economic implications are large. Even if the investment thesis is years away, the broader impact on labor markets, productivity, and how the economy functions will affect every portfolio long before specific names become buyable.

- The third act will reshape parts of the first two. Power demand, semiconductor design, and edge computing infrastructure all change when physical AI scales. Some of the first-act names that benefit today will benefit again in different ways during this phase.

What to Actually Do Right Now

For most investors, the third act is not a portfolio decision yet. The exposure that already exists through index funds and large-cap technology holdings captures most of what is worth owning at this stage.

The disciplined approach is to understand the shape of the category, identify the names worth tracking, and revisit positioning as the technology matures and the commercial deployments become clearer.

The mistake to avoid is the same one investors made in the early innings of the first act. Chasing every name that mentions the theme and paying premium valuations for unproven technology.

The Bigger Picture

Every technology cycle has a final act that is bigger than what came before. The personal computer cycle ended with the internet, the internet cycle ended with mobile, and the mobile cycle is ending with AI.

The third act of this AI cycle is the part that is most likely to produce that kind of generational impact. The disciplined approach is to stay informed, understand the trends, identify financially strong players, and wait for the commercial reality to catch up with anticipatory expectations before meaningfully sizing positions.

This concludes the three-act framework I wanted to walk through. Each act produces different winners on different timelines. The investors who do best across the full cycle will be the ones who position deliberately for the act they are in, while keeping enough flexibility to participate in the ones still ahead.