Part one of a three-part series on the phases of the AI investment cycle.

A few weeks ago, Google announced plans to invest up to $40 billion in Anthropic. The headline came and went in a day, treated as just another large number in a year full of them. But that single transaction tells you almost everything you need to know about where we are in the AI investment cycle, and almost nothing about where we are going.

A common view I see right now is treating “AI” as a single investment theme, when in reality it is at least three distinct cycles stacked on top of each other, each with different winners and different risks. Conflating them is how you end up overpaying for the wrong companies at the wrong time, even when your underlying thesis is correct.

This pattern is not unprecedented. The mobile technology cycle followed the same shape, chips and infrastructure led the market for several years before software and applications took over as the dominant winners. From roughly 2010 to 2012, the picks-and-shovels names led the way; the platforms and the application layer came later, and ultimately won biggest. Recognizing where you are in that arc matters more than picking individual stocks.

Over the next several letters, I want to walk through how I think about these phases and what each one means for how a portfolio should be positioned. Today we start with the one we are already living in.

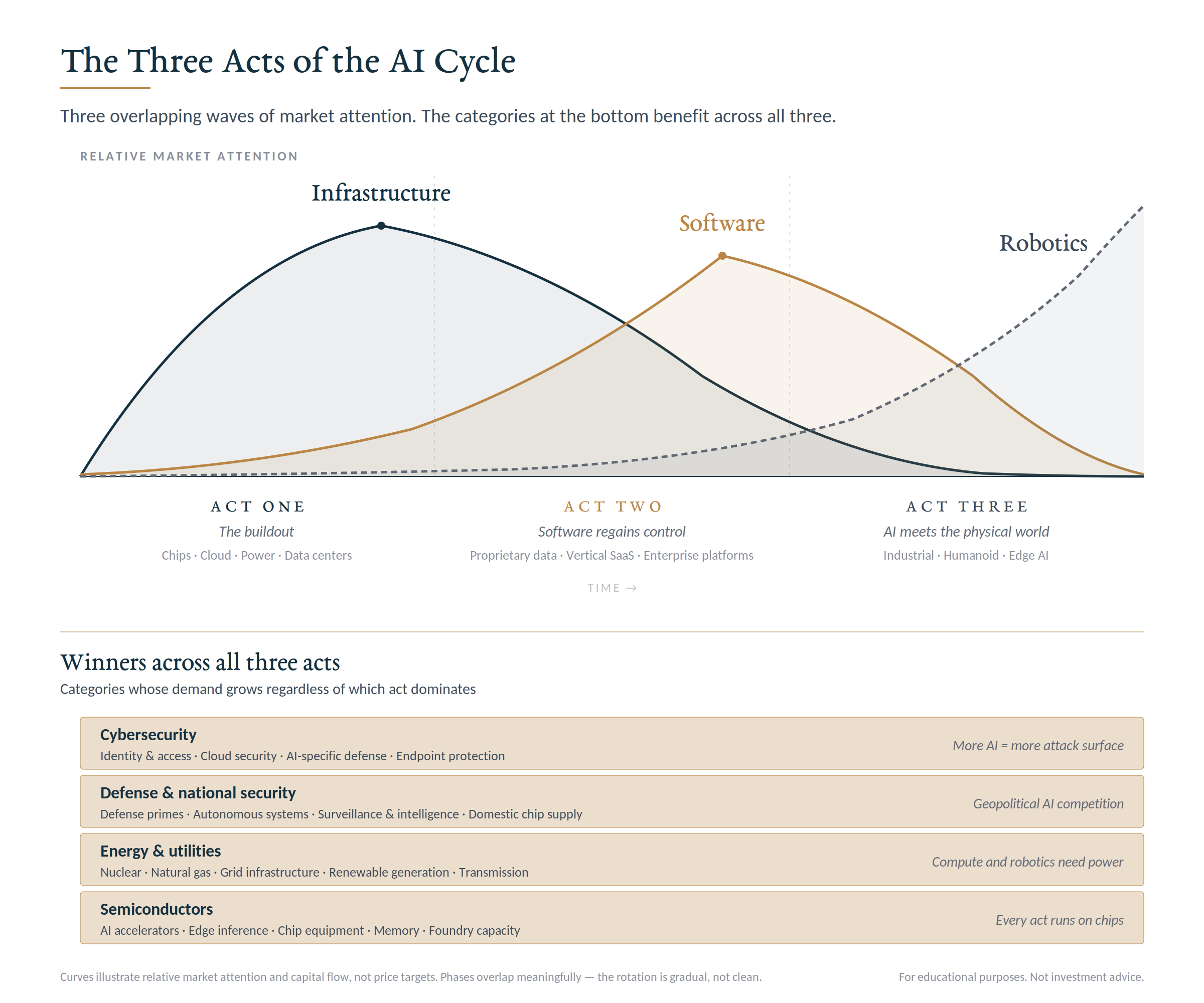

Why this matters: The companies winning today are not necessarily the companies that will win in two or five years. Each act has different leaders, and the categories at the bottom benefit across all three.

What the First Act Actually Is

The current phase of the AI cycle is not really about AI. It is about the physical and financial infrastructure required to make AI work at scale. Every chatbot conversation, every image generated, every line of AI-assisted code is the visible tip of an enormous and largely invisible buildout happening underneath. Data centers the size of small towns. Power contracts that rival what entire cities consume. Specialized chips backordered for eighteen months.

This is the gold rush phase, and the people who reliably make money in a gold rush are the ones selling shovels. The companies winning right now are not, for the most part, the ones building the AI models themselves. They are the ones supplying the picks, shovels, electricity, cooling, and real estate that make those models possible. NVIDIA is the obvious example, but the picture is much wider: hyperscale cloud providers, utilities signing decade-long power agreements, cooling and electrical equipment manufacturers, networking companies, and the firms physically building the data centers themselves.

Why This Phase Looks the Way It Does

For most of the last twenty years, technology delivered returns by being capital-light. Software companies could scale to billions of users on relatively modest infrastructure budgets. The marginal cost of one more customer was nearly zero. That is what made software the best-performing sector of an entire generation.

AI breaks that model. Training a frontier model costs billions of dollars before it generates a single dollar of revenue. Running it at scale requires power and hardware investments that look more like building a steel mill than launching a website. The companies competing at the frontier, OpenAI, Anthropic, Google, Meta, are committing to capital expenditures that, in some cases, exceed the entire annual revenue of their AI businesses.

That is why the Google / Anthropic story is so important. It is not really about Anthropic’s valuation but about a hyperscaler effectively pre-buying years of compute demand in a market where compute is the bottleneck. Every major AI announcement right now should be read through this lens.

The supporting data is striking. Reported revenue backlogs for the largest cloud providers nearly doubled year-over-year in the most recent quarter. That is not something that normally happens to fully scaled businesses, and it tells you that the demand for AI compute is not slowing, and that the buildout you read about has visibility well into the next several years.

Who Wins, Broadly Speaking

The categories benefiting from this phase share a few characteristics. They sell something physical or infrastructural that AI companies need and cannot easily substitute. They have pricing power because demand is outrunning supply, and their revenue is increasingly secured by long-term contracts with the largest and best-capitalized buyers in the world.

The categories worth understanding include:

- Semiconductors and chip equipment. The most obvious winner and also the most crowded trade.

- Hyperscale cloud and large-cap technology. The companies with the balance sheets to fund tens of billions in annual capex and the distribution to monetize it.

- Power generation and utilities. Particularly those with capacity near major data center corridors. One of the more underappreciated stories in the market right now.

- Electrical and cooling infrastructure. The unglamorous but essential equipment that makes a data center actually function.

- Networking and connectivity. The pipes that move enormous volumes of data between facilities.

- Real estate and construction tied to data center development. Specialized REITs and the builders who focus on this kind of facility.

The point is not that all of these will be winners individually but that this is where the cash is actually flowing. Understanding the shape of that flow is more useful than trying to pick the next breakout AI stock.

The Risk Nobody Wants to Talk About

The risk in the first act is not that the buildout is fake. It is happening, and the demand is genuine. The risk is one of timing. Capital expenditure on this scale has to eventually translate into cash flow that justifies it. Current valuations are pricing in a relatively smooth conversion from “we are building it” to “it is generating returns.” If that conversion gets pushed out, or happens during a period of macroeconomic stress, the same names that have led the market on the way up tend to lead it on the way down.

This is not a forecast that a correction is imminent. It is an observation that the most crowded part of the most capital-intensive theme in the market is, by definition, exposed to a particular kind of risk that does not show up in good times.

There is a related observation worth holding onto. Right now, the companies building AI infrastructure trade at premium valuations, while the software companies most likely to benefit from AI in a few years trade closer to historical averages. On a growth-adjusted basis, software multiples have already mean-reverted to the previous decade’s average. That gap is either a permanent reflection of where value will accrue, or a setup for the rotation that defines the next phase of this cycle.

It is also worth noting that the same liquidity dynamics I wrote about in the dopamine market letter last week are part of why these valuations have been sustainable for as long as they have. With trillions of additional dollars in the system looking for a home, fundamentals get to be wrong for longer than they used to. That works in both directions – it is part of why the buildout has run this long, and part of why the eventual rotation, when it comes, may happen faster than anyone expects.

What This Means for a Portfolio

The disciplined approach to the first act is not to avoid it, and not to load up on it. It is to participate thoughtfully, with a clear sense of how much exposure makes sense given everything else you own.

A few principles worth holding onto:

- Manage position sizing to account for volatility and stage of the cycle. Concentration, capex intensity, and sensitivity to capital costs make these names more volatile than the broader market. Position sizes should reflect that.

- Distinguish between exposure and concentration. Most diversified portfolios already have meaningful exposure through index funds and broad technology holdings. Adding concentrated positions on top of that is a decision worth making consciously rather than by default.

- Understand what would have to be true. For any individual position, you should be able to answer: what is this company being paid to do, who is paying them, and what would have to happen for that to slow down.

- Remember this is one act of three. The companies winning today are not necessarily the companies that will win in two or five years.

The first act is the trade you are likely already in, whether you realize it or not. The asymmetry that existed in 2023, when most investors were skeptical of the buildout, is largely gone. What replaces it is a more ordinary risk-and-reward calculation, and one that should be sized accordingly.

The Bigger Picture

The first act feels like the whole story right now because it is the story being told in the media, earnings reports, and investor letters, but it is one act of three. The infrastructure being built today is the foundation for what comes next, and what comes next will create a different set of winners in a different part of the market.

In the next letter, I want to walk through the second act, which I think is the most underappreciated part of this entire cycle, the period when the software companies most threatened by AI quietly become some of its biggest beneficiaries.

For now, the most useful thing you can do is take an honest look at your existing exposure to the first act, ask whether it reflects a deliberate decision or a passive accumulation, and make sure the size of that exposure is something you would be comfortable with in a year that is less generous than this one has been.