Many investors approach portfolio construction as if there is a correct answer waiting to be found.

How much belongs in stocks? How much should stay in cash? When should a hedge be added? What is the right amount of risk?

The problem is that markets rarely offer that kind of certainty.

That feels especially relevant today. Investors are weighing softer economic data, elevated geopolitical risk, shifting rate expectations, and a market that can change character quickly. In that kind of environment, portfolio construction starts to look less like a fixed formula and more like decision-making under uncertainty.

That is why I think humility matters so much in investing.

Not because conviction is unimportant, but conviction without humility often leads investors to overestimate what they know, underestimate what the market can still do, and hold positions too tightly once the facts begin to change.

Macro Insight

At its core, allocating capital is not about finding certainty. It is about making decisions with incomplete information.

That is one of the most useful ideas in Annie Duke’s Thinking in Bets. Good outcomes do not always come from good decisions, and bad outcomes do not automatically mean the decision was flawed. Markets are noisy, random, and results can easily fool investors who judge every decision only by what happened next.

Daniel Kahneman makes a related point in Thinking, Fast and Slow. People are wired to build stories quickly, even when the evidence is incomplete. We anchor to recent price action, overreact to headlines, and often confuse confidence with accuracy.

That is how the illusion of control enters portfolio construction.

Investors often believe that if a risk is already known, then it must already be priced in. Although, history suggests that is not always how markets work.

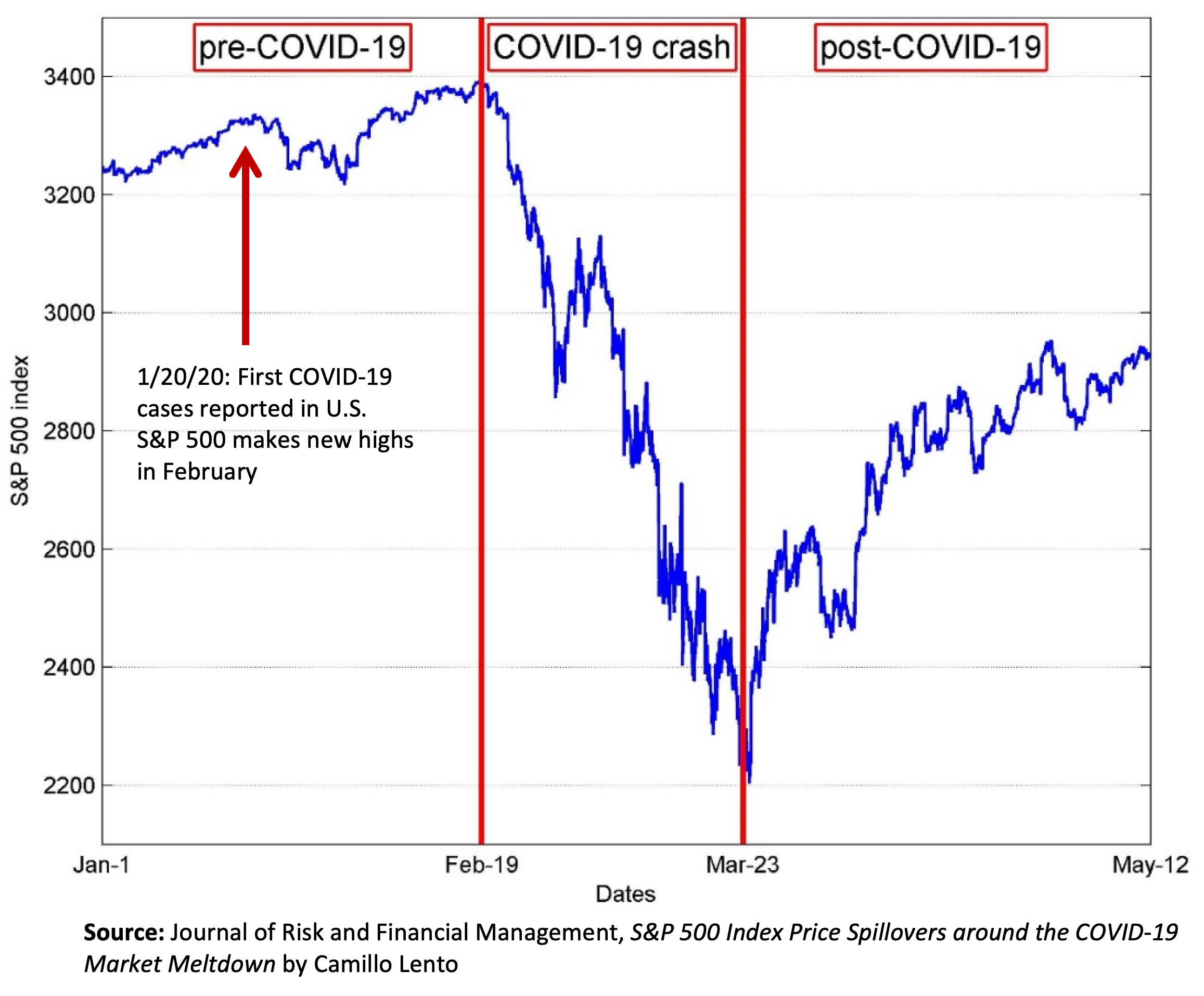

Some of the largest market declines have come well after the catalyst was already visible. COVID was identified before the market fully absorbed the economic consequences. Cracks in housing and credit were visible before the sharpest phase of the global financial crisis. Structured volatility products were widely questioned before the Volmageddon unwind. Even tariff-related risks have, at times, been discussed in advance, only for markets to react far more forcefully later.

The broader point is that awareness is not the same as full acceptance.

Markets often do not fully reprice risk until positioning changes, liquidity thins, and psychology shifts from confidence to fear.

That is one reason humility matters. Even when a risk seems obvious, the market may not have fully digested it yet.

Investment Lens

This is where portfolio construction becomes more art than formula.

When evaluating an allocation, I think a few questions matter more than investors often assume:

- What is already priced in?

- What risks is the market underestimating?

- Where are the likely liquidity zones?

- What would change the thesis?

- How much downside is acceptable if the view is wrong?

These are not questions that produce neat answers, but they can help to define risk and apply process to chaos.

Context

The same asset can mean very different things in different environments.

A long-duration bond position during a disinflationary slowdown is not the same as a long-duration bond position in a regime shaped by sticky inflation, fiscal stress, and rising term premium.

The same applies to equities. Owning growth stocks when liquidity is expanding and rates are falling is very different from owning them when inflation expectations are rising and the market is repricing duration risk.

That is why portfolio construction cannot be static. The label on the asset may stay the same, but the context rarely does.

Liquidity

Most investors spend a great deal of time on valuation and not enough time on liquidity.

Markets often move hardest around areas where positioning is crowded, stop-losses cluster, or forced buyers and sellers are likely to show up. These liquidity zones can create price moves that have little to do with long-term fundamentals and a great deal to do with market structure.

For investors, this matters because entry point and sizing still matter, even in long-term portfolios. A good idea bought in the wrong place can behave like a bad decision for much longer than expected.

Knowing when to cut a position

This is usually the hardest part psychologically.

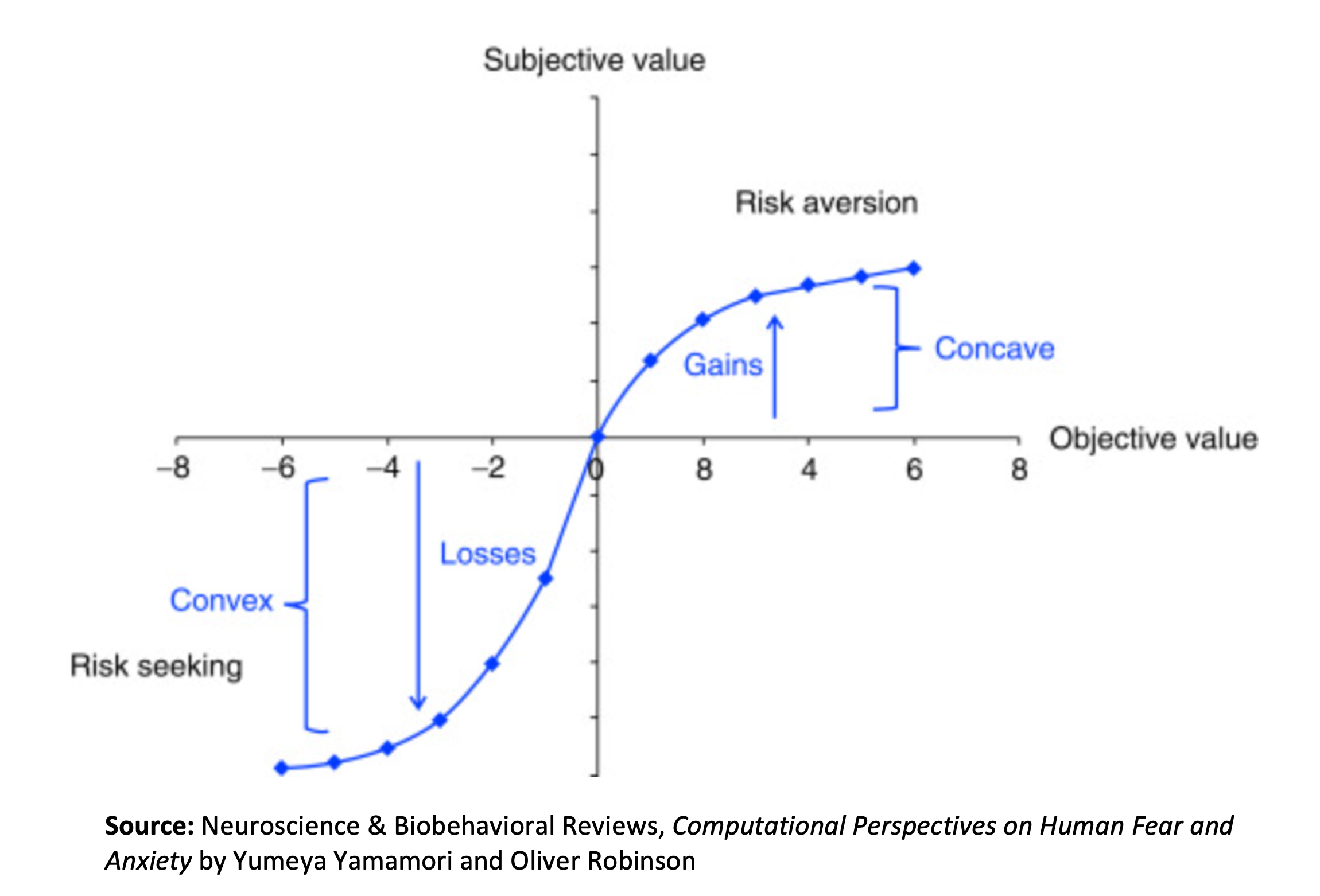

Investors often describe themselves as patient when what they are really doing is avoiding the discomfort of admitting they may be wrong. Kahneman’s and Tversky’s research on Prospect Theory has actually proven that the negative feeling of taking a loss on a position is twice as painful as the positive feeling of realizing a gain.

Sometimes the right portfolio decision is not doubling down on conviction. Sometimes it is recognizing that the facts, the market structure, or the opportunity cost have changed.

Why This Matters for Investors

Three forces make this framework especially relevant today.

1. Markets are being driven by competing narratives

Investors are weighing inflation risk, slower growth, geopolitical stress, and policy uncertainty at the same time. That creates an environment where leadership can change quickly and reversals can be sharp.

2. Known risks are not always fully priced

One of the market’s recurring mistakes is assuming that because a risk is visible, it has already been fully discounted. In reality, markets often accept risk only gradually, and sometimes all at once near the end of a move.

3. Portfolio construction is increasingly about trade-offs

There is no perfect allocation in a market where inflation, growth, liquidity, and geopolitics are all moving at once. Instead of attempting to achieve certainty, portfolio management is more about balancing competing risks without becoming overconfident in any single outcome.

At Roundtable, I think one of the most underappreciated parts of portfolio management is knowing how much confidence to have, and how much flexibility to preserve.

A portfolio should reflect conviction, but it should also reflect humility.

That means sizing positions based on probabilities rather than narratives. It means respecting liquidity and market structure, not just long-term valuation. It also means knowing in advance what evidence would lead us to reduce, add to, or exit a position.

In practice, that can mean:

- Holding smaller positions when the idea is attractive but the backdrop is unstable

- Adding only when price, liquidity, and thesis are aligned

- Reducing positions when the original rationale no longer holds

- Treating cash as optionality rather than inactivity

The goal is not constant activity but clearer decision-making under uncertainty. That is often what separates durable portfolio construction from simple conviction.

The Bigger Picture

Portfolio construction is part science and part art.

It requires data, discipline, and a repeatable process. It also requires judgment. Investors are constantly balancing competing dynamics: inflation against growth, conviction against humility, patience against denial, and long-term value against near-term liquidity.

There is no single right answer.

There are only better and worse ways to make decisions when certainty is unavailable.

That is why I think the best portfolios are built with humility. Not because humility makes investors passive, but because it makes them realistic. Markets, and risk, are not binary, and control is often much more limited than it appears.

The investors who manage capital best over time are usually not the ones who claim certainty. They are the ones who think in probabilities, update quickly, and understand that even widely known risks can be repriced much later than expected.

Good portfolio construction does not come from pretending to know exactly what happens next.

It comes from staying adaptive when the facts, and the market’s reaction to those facts, begin to change.