For the last two years, the AI trade felt unusually straightforward.

Own the companies spending the most, building the most data centers, and buying the most chips. Markets rewarded scale, speed, and ambition.

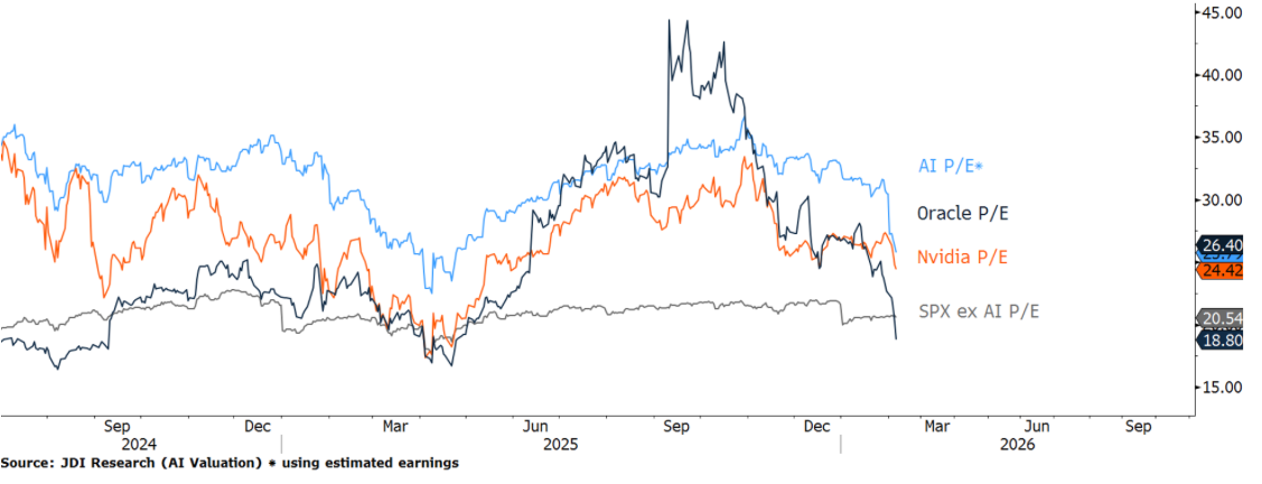

The long-term AI trajectory still feels real, but the stocks tied most directly to that narrative have weakened substantially, even as spending has remained robust. That creates a real tension: if the theme still makes sense, why are the leaders struggling?

The answer, I think, is that the market is beginning to separate the long-term promise of AI from the shorter-term reality of owning these stocks in a more difficult macro environment.

In a strong growth backdrop, markets will often reward spending long before returns arrive. In a weaker, more disinflationary environment, investors become less patient. They want evidence of earnings durability, disciplined capital allocation, and more immediate payoffs.

That is where I think the AI trade is starting to change.

Macro Insight

I think the cleanest way to frame the current moment is that the market is shifting from rewarding AI ambition to demanding AI economics.

On one hand, the long-term case for AI still looks compelling. On the other hand, the stocks that led the first phase of the rally were priced for a world in which spending itself was enough to justify higher valuations.

There are two main reasons that has become harder to sustain.

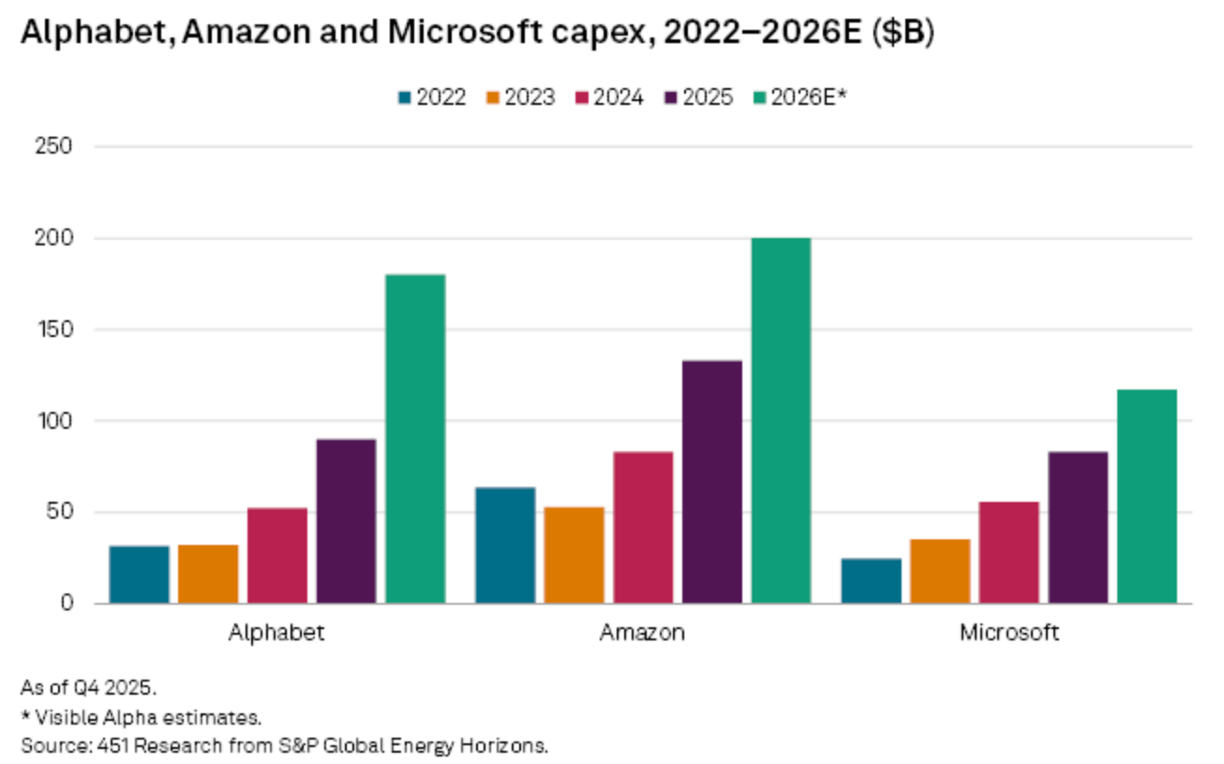

1. Hyperscaler spending is still strong, but investors are starting to question the payoff.

Alphabet, Amazon, and Microsoft alone guided to roughly $495 billion of capex for 2026, up sharply from 2025, with much of that tied to AI infrastructure. That spending may continue for some time, but the market appears less willing to treat every new capex plan as proof of deeper moat or future dominance.

2. The macro backdrop is becoming less supportive.

The Iran war has created an inflationary impulse through oil and gas, but I do not think investors should assume that lower rates, if they eventually arrive, will come for good reasons. Rates may fall later not because growth is reaccelerating, but because the underlying economy is weakening enough to push the market into a more clearly disinflationary regime.

Tech and AI names can see relief rallies when rates start to roll over, but if those lower rates are being driven by economic weakness rather than healthier growth, those rallies can be brief. A weaker economy can still pressure earnings, enterprise spending, and investor willingness to pay premium multiples.

The real question is not whether AI will matter over time. It is whether the market still wants to pay top-tier valuations for companies spending aggressively as growth softens.

Once inflation cools for constructive reasons and growth stabilizes, the market is more likely to reward the companies with the best underlying economics.

Investment Lens

This is where I think investors need to separate AI into two buckets:

- the infrastructure builders

- the AI beneficiaries

The infrastructure builders

The hyperscalers are obviously key components of future growth. They own cloud relationships, massive customer bases, and much of the compute stack.

If several of the largest companies are all spending aggressively on similar AI infrastructure at the same time, then the spending itself becomes less differentiated. Scale still matters, but sheer capex becomes a weaker moat when everyone at the top is racing to build.

The issue shifts from who is spending the most to who will actually earn attractive returns on all of that spend.

That is why lower valuations alone do not automatically make these names obvious buys here.

The beneficiaries

The more interesting long-term winners may be the companies that benefit from AI adoption without bearing the full cost of the infrastructure race.

A company like Apple is one example. Apple has not led the AI capex arms race, but it still controls one of the most valuable distribution layers in the world: the device, the operating system, and the customer relationship.

A helpful analogy is refrigeration and Coca-Cola. Refrigeration changed the economics of beverage distribution and consumption, but the long-term winner was not simply the company that manufactured the refrigerator. Coca-Cola benefited because it controlled the brand, the shelf presence, and the customer relationship once the infrastructure became widely available.

AI may work similarly. The more durable winners may be the businesses that use hyperscaler infrastructure to strengthen distribution and capture economics at the point of consumption.

Why This Matters for Investors

Three things matter here.

1. The market is becoming more selective about AI capex

The first phase of the AI trade rewarded scale and ambition. The next phase is likely to reward monetization and return on invested capital.

2. Lower rates may not be enough on their own

If rates fall later this year, it may not be because the environment is turning healthy again. It may be because growth is slowing enough to force a more defensive market backdrop.

3. Existing tech positions need a different framework now

This is no longer just a momentum trade. Investors need to think more carefully about what they own, why they own it, and what part of the AI value chain they are actually exposed to.

At Roundtable, I think the practical takeaway is to avoid treating AI as one trade. For existing positions, I would focus on three questions:

- Is this company still benefiting from a strong underlying earnings trajectory, or is the position relying mostly on the idea that rates may eventually come down?

- Where does the company sit in the value chain? Is it bearing the cost of the buildout, or benefiting from the buildout?

- If fresh capital is going into the theme, is it being added into weakness that reflects improving long-term value, or simply into a relief bounce inside a broader downtrend?

If the market moves deeper into a risk-off, disinflationary regime, I think investors should be open to the idea that the best AI opportunities may not come from buying the biggest infrastructure spenders first.

At the same time, fresh capital may ultimately be better directed toward businesses that:

- control customer access

- can integrate leading models without building the entire stack

- can improve margins through AI adoption

- benefit from AI demand without taking on the full capex burden

That is a different mindset from what worked in the first leg of the AI trade, but I think it is the right one now.

The Bigger Picture

AI is not going away, but the investment case is changing. This is becoming less of a story about who can build the biggest cluster of GPUs and more of a story about who can convert AI into durable economics in a tougher macro environment.

Lower rates could certainly help tech stocks bounce, but if those lower rates arrive because the economy is weakening, the relief may prove temporary. A weaker economy can still pull down earnings expectations, pressure multiples, and force investors to become more selective inside the sector.

So are AI leaders attractive buys here?

Some may be getting closer, but I think investors should become more selective, patient, and focused on business model quality than on capex alone.

The next winners in AI may not be the companies spending the most.

They may be the ones best positioned to benefit after the spending wave stops impressing the market.