For most investors, a sustained closure of the Strait of Hormuz would mean one thing: higher oil prices.

That is the obvious conclusion, but not necessarily the most interesting investment opportunity.

The Strait of Hormuz is one of the world’s most important energy chokepoints. It is a critical route not only for crude oil, but also for the feedstocks and trade flows that shape fertilizer, chemicals, and agriculture.

That matters because some of the most interesting beneficiaries of an extended closure may not be oil producers at all.

Three areas stand out:

- Fertilizer producers with secure North American gas access

- American chemical companies that gain relative cost advantages as overseas peers face tighter feedstocks

- Grain merchants and ag traders that benefit from volatility, dislocation, and changing crop economics

The common thread is that all three sit one step removed from the immediate headline, but in some ways may have better economics, and upside, if the disruption lasts.

Macro Insight

The key idea here is that although a Hormuz closure is an oil shock, it should really be viewed as an input-cost shock.

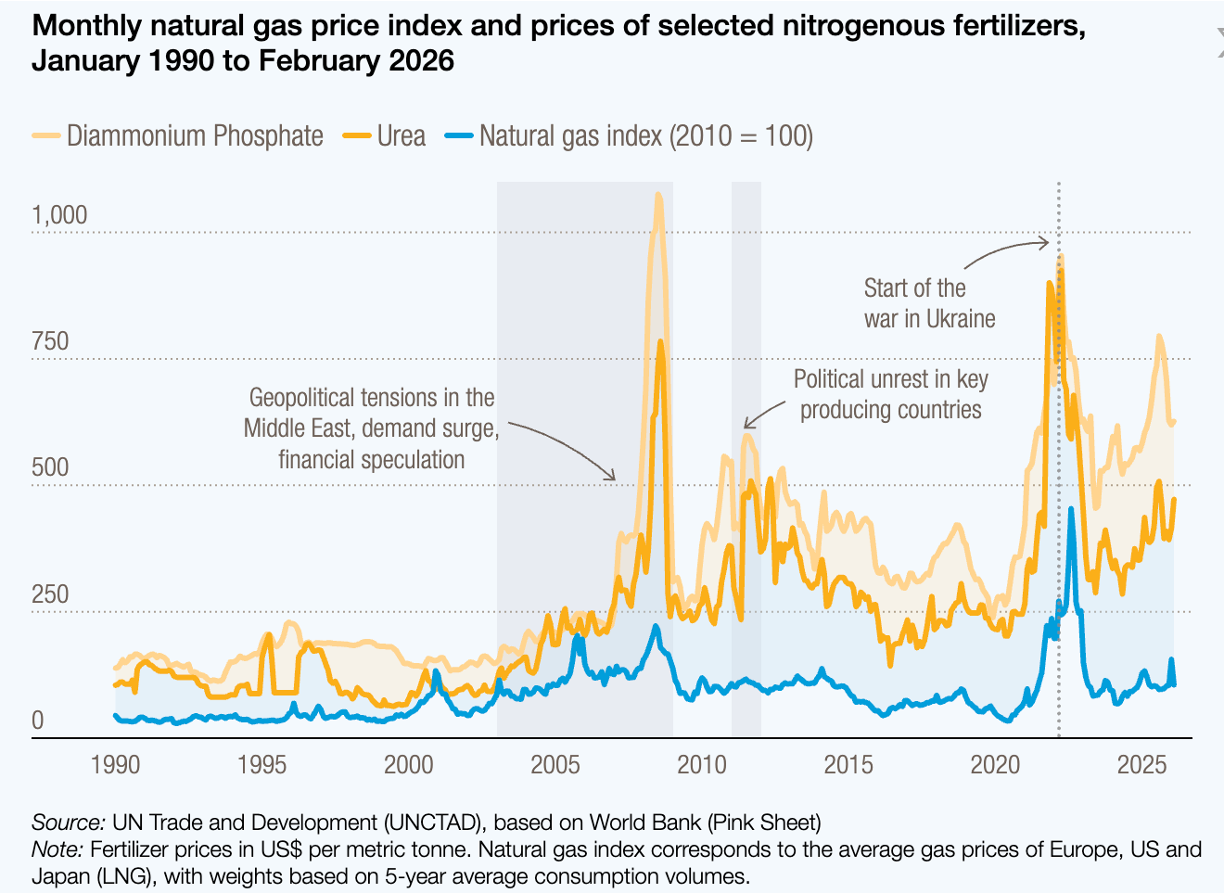

Most investors understand the crude link, but fewer focus on liquified natural gas, or LNG. In 2024, roughly one-fifth of global LNG trade passed through the Strait of Hormuz, with Qatar alone exporting about 9.3 billion cubic feet per day through that route.

This is important because natural gas is a core industrial input, not just an energy source.

Why fertilizer responds

For one, nitrogen fertilizer is highly sensitive to gas prices.

CF Industries notes that natural gas is the principal raw material and primary fuel source used in ammonia production and accounts for roughly 70% of the cost to manufacture ammonia. Ammonia is the building block for products such as urea and UAN.

If LNG flows are disrupted and global gas markets tighten, fertilizer prices tend to respond quickly.

Why chemicals respond

The same logic applies to chemicals.

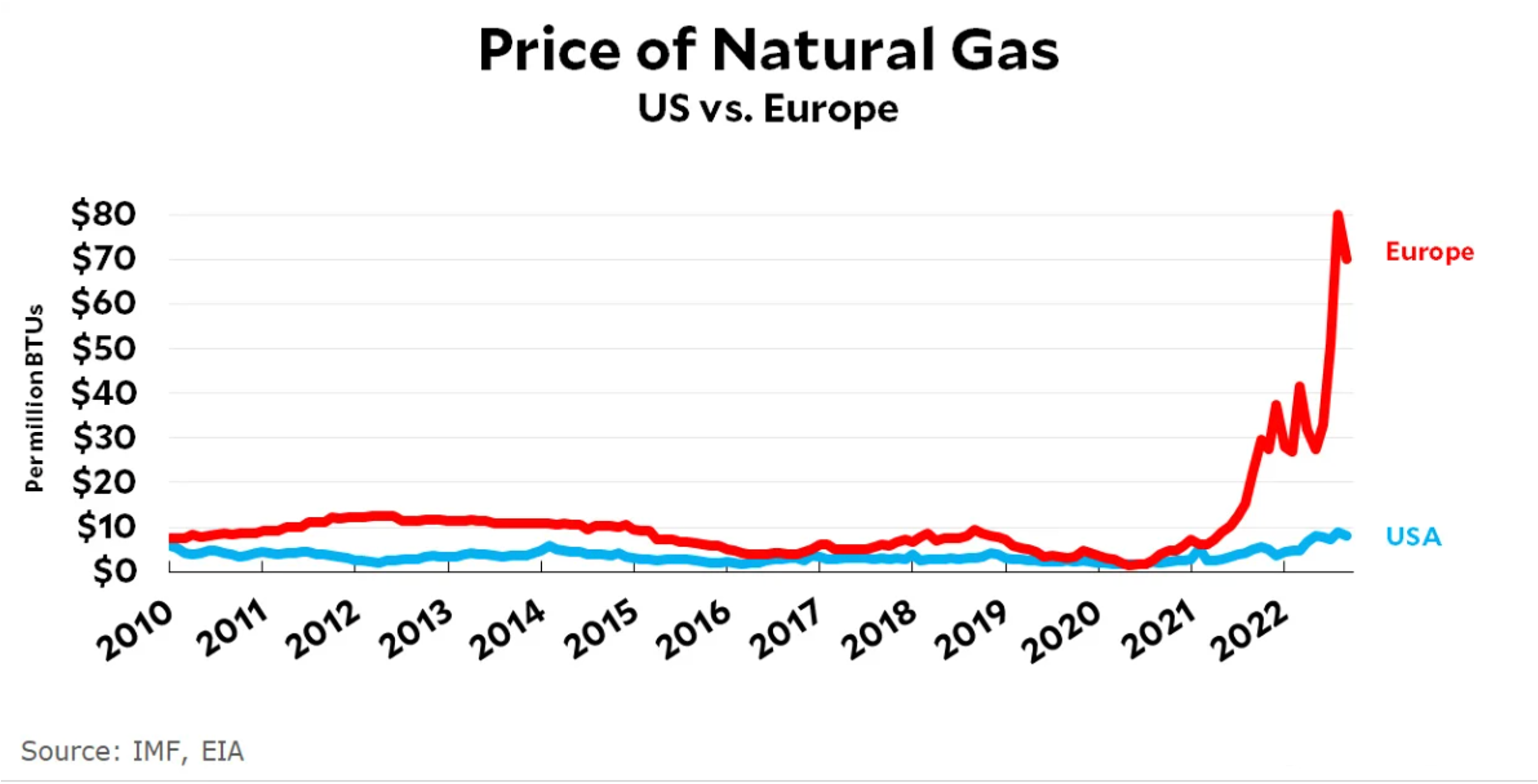

Many chemical production chains rely on natural gas or natural gas liquids as feedstocks. When those inputs become scarcer or more expensive, producers with secure low-cost domestic supply gain a relative advantage over international competitors.

That is one reason high energy costs have been such a persistent problem for Europe’s chemical industry. For example, Dow recently closed multiple European chemical plants in response to structurally high costs and weak competitiveness in the region.

Why agriculture responds

From there, the shock moves into agriculture.

Higher fertilizer costs raise farm input costs. Higher diesel costs raise transportation and equipment costs. Trade route disruption then adds another layer of volatility to crop merchandising and global grain flows.

That combination is how an energy chokepoint becomes a broader commodity and supply-chain event.

Investment Lens

The market’s first instinct in a Hormuz shock is usually correct but incomplete.

Yes, oil likely rises. But the more practical investment question is:

Who benefits when critical inputs become scarcer and more expensive?

1. Fertilizer companies

This is probably the clearest second-order winner.

Ammonia production is highly sensitive to natural gas because gas is both the principal feedstock and a major energy input. That is why disruptions to LNG and gas markets can quickly feed through to nitrogen fertilizer pricing.

If LNG markets tighten and gas-linked fertilizer costs move higher, producers with secure North American supply should become more advantaged.

That is why names like Nutrien, Mosaic, and CF Industries stand out.

The point is not that demand suddenly changes. It is that the global cost curve shifts, and producers with stable access to key inputs become more valuable.

2. American chemical companies

The chemical thesis is a little more nuanced, but I think it is still compelling.

Many foreign chemical producers already operate with a weaker feedstock position than U.S. companies. If a Hormuz disruption pushes gas and energy-linked inputs higher, that relative disadvantage likely gets worse.

That creates a better setup for U.S. names such as Dow, LyondellBasell, and AdvanSix, particularly in commodity and intermediate chemical chains where feedstock cost is a major driver of margins.

This is not a blanket bullish call on chemicals. Demand still matters, but in a world of tighter global energy-linked inputs, I do think American producers become better positioned relative to overseas competitors.

3. Grain merchants and agricultural merchants

This is probably the least obvious part of the thesis, which is why I find it interesting.

At first glance, higher fertilizer and diesel costs sound negative for agriculture. And for farmers, they often are.

But companies like Bunge, ADM, and The Andersons are not just directional bets on crop prices. They are merchandising, processing, storage, and logistics businesses that can benefit when volatility increases and trade flows become less efficient.

When input costs rise and crop economics begin shifting across regions, these merchants can often make more money through origination, storage, basis trading, and changing trade routes.

So, while the market may start with oil, I think grain merchants have a real chance to be among the more interesting beneficiaries if the disruption is prolonged.

Why This Matters for Investors

Three macro forces make this setup especially relevant.

1. Energy shocks create pricing power outside energy

When LNG and gas-linked inputs tighten, fertilizer and chemical producers with advantaged supply can gain pricing power or improved relative margins.

That matters because second-order winners often outperform the obvious first-order trade once markets begin to price the full system impact.

2. Input inflation travels downstream

A Hormuz closure would not stay contained to crude.

Higher fertilizer, diesel, and feedstock costs feed into agriculture, industrial production, and transport. Investors should think not only about commodity scarcity, but about who can pass those costs through and who can profit from tighter markets.

3. Volatility benefits intermediaries

Periods of trade disruption often reward the companies that sit between production and end demand.

That is why grain merchants and ag processors can be compelling in this framework. The winners are not always just the producers of scarce commodities. They are often the intermediaries best positioned to navigate fragmented markets.

At Roundtable, I think the practical way to approach a geopolitical shock like this is to avoid stopping at the obvious conclusion.

Oil may absolutely be part of the story, but if the disruption lasts, I would be more interested in the businesses whose relative economics improve as global inputs tighten and trade flows become more fragmented.

That includes:

- Fertilizer producers with secure North American gas access

- U.S. chemical companies whose overseas competitors move further up the cost curve

- Grain merchants that can monetize volatility and shifting trade patterns

The broader principle is that some of the better opportunities often sit one step away from the immediate headline.

That is usually where the thesis becomes less crowded and, in many cases, more durable.

The Bigger Picture

The larger point is that global chokepoints do not just affect commodities. They affect cost structures, trade flows, and competitive positioning across industries.

A prolonged Hormuz closure would not simply be an oil story. It would also be a story about LNG, fertilizer, chemical margins, diesel inflation, and agricultural merchandising.

That is why I think the more interesting opportunities may sit outside of traditional energy.

Everyone will see crude, but fewer investors spend enough time on the companies that benefit when global inputs become scarcer, trade flows become less efficient, and volatility moves up the supply chain.

That is often where the more interesting opportunities are found.