Why power, and the equipment that delivers it, may matter more than the chips.

During any conversation about AI these days, the most common topic that dominates is chips and the companies that make them. This makes sense given the rise in the share prices of Micron, SanDisk, and Marvell, but the more I look into where the real constraint for AI sits, the less sure I am that chips are still the binding one. What keeps coming up in my research is not chips, but electricity, and whether we can produce and move enough of it. Most of the technologies we are excited about, AI, robotics, advanced manufacturing, even space, depend almost entirely on energy, and AI is the one already pushing against the limits of what the grid can supply. It is also the one where the cost of power gets passed through, almost immediately, into the price of every answer the model produces.

The significance of this goes beyond AI because growth and energy tend to move together. It is hard to build, transport, or compute without turning power into something useful, so when energy is cheap and available the economy has an easier time, and when it is not, growth gets harder. In a country carrying a lot of debt, the cleanest way out is to grow faster than the debt does, which is one more reason power has been on my mind.

Where the Buildout Gets Stuck

For most of the past forty years, U.S. energy demand grew slowly. Efficiency gains roughly offset rising consumption, and the grid was treated as mature infrastructure. AI changed that in a single cycle, with data center power demand expected to roughly double by 2030. In the regions where the buildout is concentrated, demand from the likes of Microsoft, Amazon, and Google is already outpacing what the grid can supply. The constraint is not chips, it is not capital, and it is not talent. It is power, and more specifically the ordinary equipment that moves it from the grid to the rack.

Data center location used to be about fiber and proximity to users. Now the first question is whether there are megawatts available, and some operators have stopped waiting on the grid and started building their own generation on site. The piece of hardware most likely to hold up a multi-billion-dollar facility is not a processor but the large transformer that steps grid power down to the voltage a data center can use. Lead times on those now run up to five years, and the same shortage delays the grid upgrades that would relieve them. A site can have its money committed, its chips allocated, and its building finished, and still sit dark waiting on a part, and projects that were already greenlit are starting to slip or get cancelled outright.

Power is the biggest operating cost in a modern AI data center and now the biggest obstacle to building one, and every answer a U.S. model produces carries that cost with it.

Why It Is Cheaper to Run AI Elsewhere

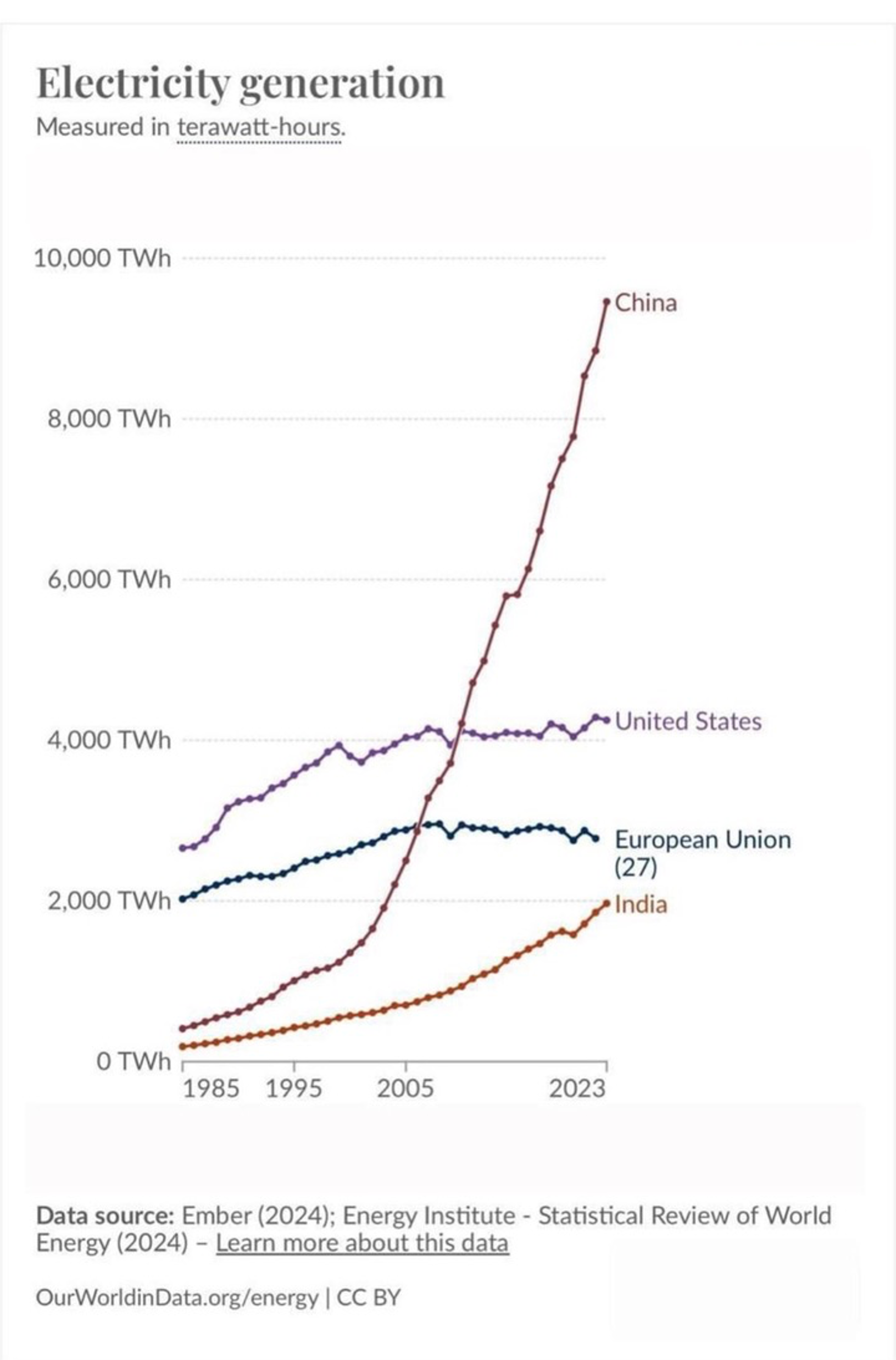

All of this would matter less if the rest of the world had the same problem, but it does not. China now generates more than twice as much electricity as the United States, and the gap keeps widening.

Why this matters: Whichever country has the cheapest, most abundant power can run AI at a lower cost, and that advantage compounds with every model deployed.

Cheap, plentiful power is not the only reason Chinese AI is cheaper to run, but it is one of the biggest, and the hardest to fix because building generating capacity takes years. China is adding new power capacity at many multiples of the U.S. rate, across renewables, nuclear, and coal alike, while U.S. additions have crept along. American models are still the most capable, but the lead is shrinking fast, and the alternatives cost far less to use.

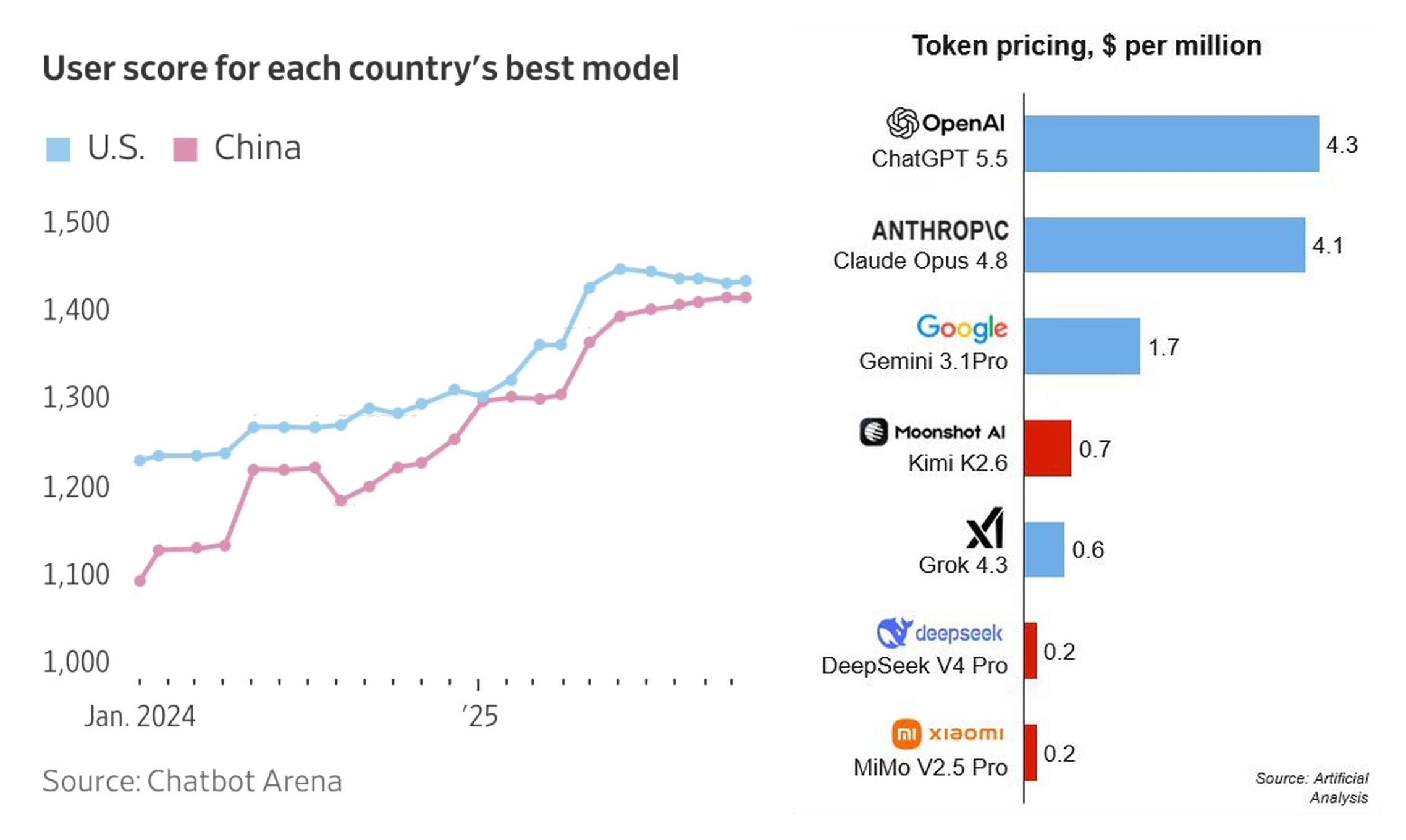

Why this matters: Quality is converging while price is not. When a Chinese model is nearly as capable and costs a fraction of its U.S. counterpart, the commercial winner is decided on cost rather than capability.

The quality gap between the best U.S. and Chinese models has narrowed from about 140 user-rating points to roughly 20 in under two years, while the top Chinese models charge a fraction of the price. For a lot of real uses, the model that wins is not the most capable one, it is the one that is good enough at the lowest price. The U.S. still leads in chip design, capital markets, and software, but power has become the variable a lot of the race runs through.

The Bigger Picture

The AI story is not really about chips, it is about power, and the data center is where that becomes concrete. Every gigawatt of new generation, every mile of new transmission, and every transformer coming off an American factory floor is part of whether the U.S. keeps pace because the country that can put the most power to work at the lowest cost will set the price of intelligence for the rest of the world.

That reframes where the next few years of returns may actually come from. Energy supply, long treated as a sleepy defensive corner of the market, sits underneath almost every technology we are counting on for growth. The businesses that generate, store, and move electricity, including the unglamorous ones making the gear that connects a building to the grid, are likely to matter as much as the ones writing the code on top. This means widening the lens beyond chips, because the same buildout that drove the chip story for the past two years is starting to hit a wall the chip story cannot get past on its own, and what comes next will be decided one transformer and one power plant at a time.