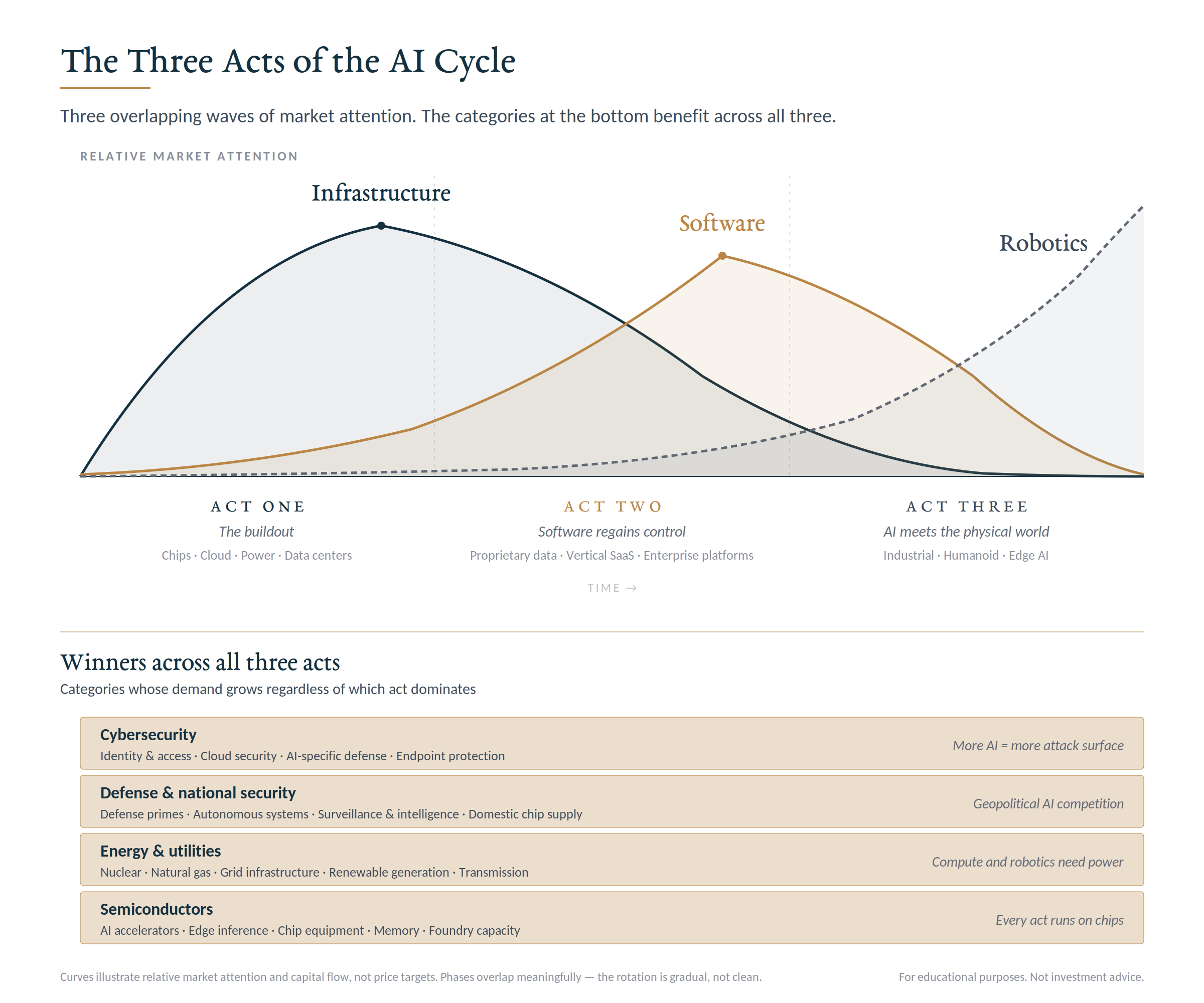

Part two of a three-part series on the phases of the AI investment cycle.

Over the last two years, AI has looked like a story about chips, data centers, and the handful of companies building enormous foundation models. That has been the first act of a multi-year journey, and it has been the right place to be invested, but I don’t believe it is where this cycle ends.

The second act is harder to see because it is the opposite of the current consensus. Enterprise software, the consensus view holds, is the obvious casualty of AI. If AI can write code, generate reports, and manage workflows, then the companies that did those things should no longer have a future.

I think this consensus view is half right, but software companies are more than applications and code. Maximizing their well-established moats is where the next several years of opportunity probably lives.

Why this matters: We are entering the rotation point where the first act’s leaders give way to the second act’s beneficiaries. Recognizing where you are in this arc is the practical work of the next several years.

Why Software Looks Like a Loser Right Now

Software valuations reflect the consensus view. On a growth-adjusted basis, enterprise software valuations have already mean-reverted to the previous decade’s average, with many high-quality companies trading at the lowest multiples they have seen in years.

The market’s reasoning for these discounts makes sense. AI commoditizes the production of software. Writing code is genuinely getting cheaper and more efficient than it has ever been, lowering the barrier to building basic tools that streamline operations for businesses. If the only moat a software company has is the difficulty of building the software itself, then that moat is shrinking.

Although, the best enterprise software companies were never really competing on the difficulty of building software. They were competing on something harder to replicate.

What Software Companies Actually Own

The thing that separates a great enterprise software company from a mediocre one is rarely the code. It is the proprietary data the code generates and structures over time.

Companies like Workday, ServiceNow, Salesforce, and Veeva hold the actual records across their respective domains for thousands of large enterprises. This proprietary data across areas like Finance, HR, Sales, IT, and Compliance is untouchable by current AI models and public domains. The most powerful AI model in the world cannot tell a CFO whether their company’s expense approval cycle is faster or slower than their industry peers, because that comparison data simply does not exist outside the systems where it was generated.

When an AI model gets layered on top of that kind of data, the output is different from what consumer AI products produce. Instead of a generic response to a generic prompt, specific business problems can receive targeted answers that are informed by data nobody else has access to.

The second advantage, which is underappreciated in my view, is that the customers paying these companies are already paying them. They have signed contracts, integrated these systems with everything else they run, and built their actual workflows around these tools. When ServiceNow launches AI-powered features, they do not have to convince a CIO to buy ServiceNow. They just have to convince the CIO to upgrade. That is a fundamentally different sale than what an AI startup is making, and it explains why these companies can monetize AI faster than many venture-backed names.

One example of how software companies have recognized this and are acting on it today is the recent announcement by Salesforce that they are increasing their sales staff by 20%. This is a direct counterweight to the job displacement happening in other departments, and it demonstrates where their moat really lies: their ability to retain and upsell customer relationships.

The Gap Between Story and Value

When looking at how these companies fit into a portfolio, step back and look at what is actually happening in the market. Infrastructure companies trade at premium valuations on the assumption that AI will generate enormous value. Software companies trade at average or below-average valuations on the assumption that AI will commoditize them, with IGV (iShares Expanded Tech-Software ETF) down roughly 21% for the year and software stocks now trading at a discount to the S&P 500 for the first time in modern history.

The key here is that infrastructure cannot create economic value on its own. Compute is a critical input, but the real value comes from what it powers. The enterprise mainframe was declared obsolete every decade since the 1970s, but the companies running on it kept generating value because the integration with customer operations was the actual moat. The companies actually putting AI to work, running it on real data, embedding it in workflows, monetizing it through customer relationships, are largely the enterprise software incumbents. They are the ones with the customers, the data, and the distribution to turn AI capability into revenue.

What This Means for a Portfolio

The disciplined approach to the second act looks different from the first.

A few principles worth holding onto:

• Quality of moat matters more than AI narrative. As with any investment, digging into the fundamentals of the specific companies is important. Not all software companies are built alike. The ones best positioned will own data and workflows that AI makes more valuable.

• Time horizon should match the thesis. This is a multi-year setup, not a quarterly trade. The catalysts that would force a re-rating are happening, but unevenly, and the rotation may take longer than feels comfortable.

• Be careful with AI-first names. The companies most aggressively marketing themselves as AI-native often have the weakest data moats. The likely winners of the second act are more often names that have been quietly compounding customer data for years.

The Bigger Picture

Every investment cycle produces a moment where the consensus view shifts in a dramatic and durable way. The companies that look threatened in the early innings are often structurally well-positioned for the later ones. What looks like a threat from the outside is usually happening on top of an asset the disruptor cannot easily replicate (e.g., a customer relationship, dataset, or workflow).

The first act of this cycle rewarded companies building the foundation. The second act probably rewards the companies building on top of it.

In the next letter, I want to walk through what comes after software has its turn, the period when AI begins to merge with the physical world through robotics, autonomous systems, and other hardware. That is further out, but it is worth understanding now because it will likely have some of the more significant impacts to daily life.

The opportunity in the second act is to anticipate where the market is wrong. Right now, it has stopped distinguishing between companies that should be marked down and companies that should not. Telling the difference is the work.