For much of the past decade, one investment philosophy dominated discussions about portfolio construction: passive investing.

Following the global financial crisis, low interest rates, stable inflation, and an extended bull market in equities created an environment where simply buying and holding broad market indices proved remarkably effective. Index funds attracted trillions of dollars, and the philosophy of “stay invested and ignore the noise” became widely accepted.

But the environment that supported this approach may now be changing.

Interest rates have risen meaningfully from their post-crisis lows. Government debt levels are expanding. Geopolitical tensions have increased. And technological disruption is reshaping industries at an accelerating pace.

Together, these forces are contributing to an important shift in financial markets: volatility is returning.

For investors, this raises an important question.

If the past decade rewarded passive exposure to steadily rising markets, what investment approach works best when markets become less predictable?

Macro Insight

Passive investing works best in environments where economic conditions are stable and markets trend steadily upward over long periods of time.

The years following the 2008 financial crisis offered exactly that environment. Central banks kept interest rates near zero, inflation remained subdued, and liquidity flooded global financial markets.

These conditions supported a powerful expansion in equity valuations. As index funds absorbed increasing inflows, the largest companies within major indices benefited the most, reinforcing the momentum of passive investing.

But market environments rarely remain stable indefinitely.

Today, several structural forces are introducing greater uncertainty into the global economy:

- higher interest rates

- rising fiscal deficits

- geopolitical fragmentation

- rapid technological disruption

Each of these forces has the potential to increase the frequency and magnitude of market volatility.

Historically, environments characterized by higher volatility tend to reward investors who can adapt portfolios dynamically rather than simply maintain static exposures.

In this context, volatility does not necessarily need to be feared.

In the right framework, volatility can become a source of opportunity.

Investment Lens

The idea of benefiting from volatility rather than avoiding it comes from a concept popularized by Nassim Nicholas Taleb in his book Antifragile.

Taleb describes three types of systems:

- Fragile systems, which break under stress

- Robust systems, which withstand shocks but do not benefit from them

- Antifragile systems, which actually improve when exposed to volatility and uncertainty

Most traditional investment portfolios are designed to be robust. They aim to survive market downturns while participating in long-term economic growth.

Antifragile portfolios take a different approach.

Instead of assuming stability, they recognize that volatility, regime shifts, and unexpected shocks are inherent features of financial markets.

Rather than attempting to eliminate volatility entirely, antifragile strategies seek to structure portfolios so they can benefit from market dislocations and sudden shifts in expectations.

One of the most practical frameworks Taleb outlines for achieving this is known as the barbell strategy.

The Barbell Approach

The barbell strategy separates a portfolio into two very different components: an “extreme safety” side and a “high convexity” side. The middle — moderate risk with moderate upside — is largely avoided.

Below are examples of what a barbell can look like across equities and fixed income.

The purpose of this structure is simple: the safe side protects against catastrophic loss, while the opportunity side preserves upside when markets move sharply. This combination limits downside while preserving the ability to capture upside created by volatility.

Why This Matters

In a higher-rate world, diversification is not just about owning different assets — it is about understanding how those assets behave when inflation and rates move quickly.

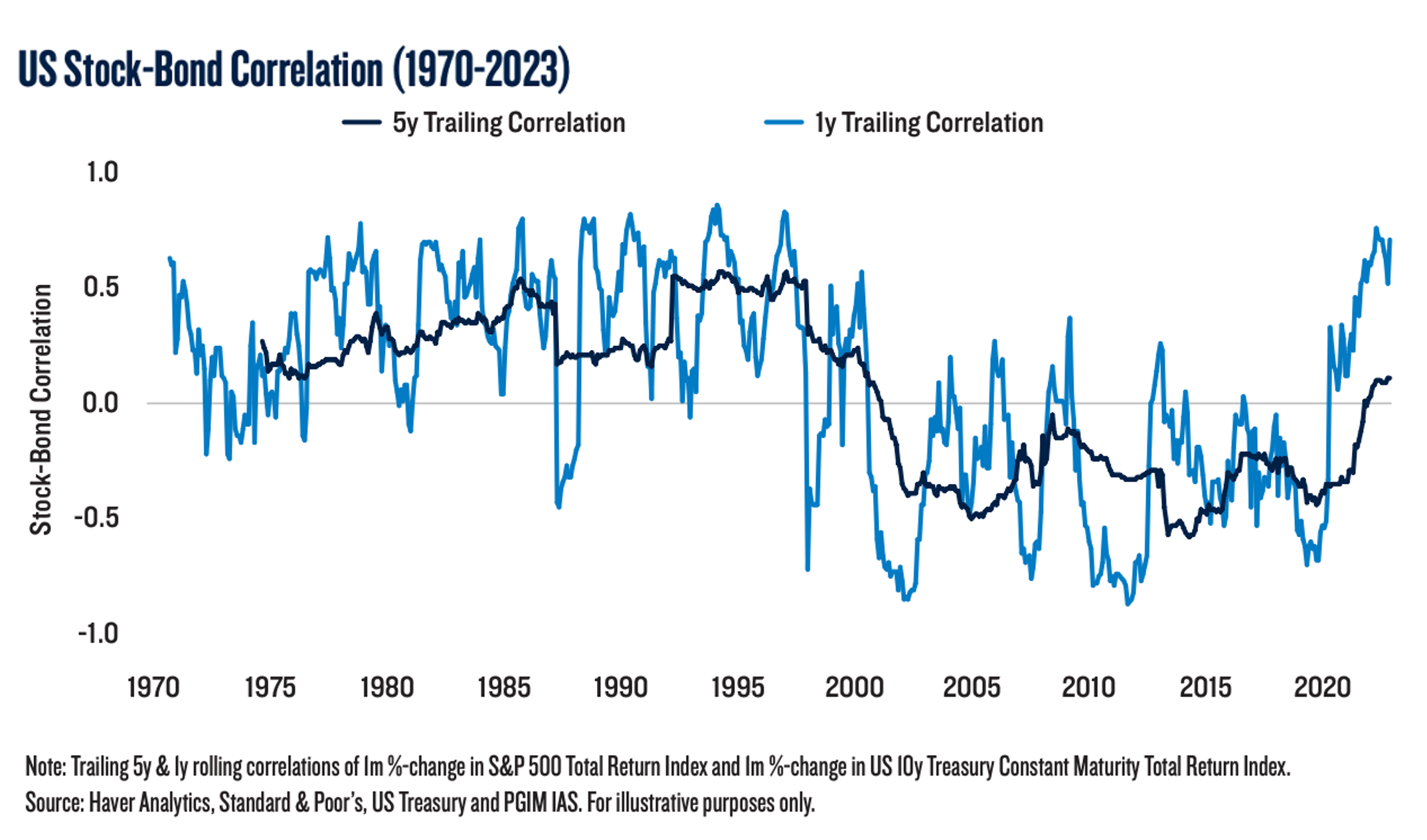

One way to see this is through stock-bond correlation. When stock-bond correlation rises, the classic “stocks down / bonds up” assumption becomes less reliable — and portfolios need broader tools for resilience and opportunity.

Against that backdrop, three forces help explain why the passive playbook can feel less reliable — and why antifragile design matters:

1. Interest Rate Volatility

Interest rates now play a much larger role in determining asset prices than they did during the era of near-zero rates. Changes in inflation expectations and central bank policy can rapidly shift market leadership across sectors and asset classes.

2. Economic Regime Changes

The global economy appears to be transitioning from a period defined by ultra-low interest rates and globalization toward one characterized by higher borrowing costs, geopolitical competition, and technological disruption. These transitions can produce sudden changes in which sectors or strategies outperform.

3. Market Concentration

Passive investing has increasingly concentrated capital in the largest companies within major indices. When market leadership shifts, concentrated markets can experience sharper rotations than investors may expect. In this type of environment, investors who can adjust portfolio positioning as conditions evolve may have an advantage over purely static approaches.

Antifragility in a portfolio context is not about prediction — it is about structural design.

An antifragile portfolio does not merely withstand volatility; it is constructed so that it can improve its position when volatility increases.

At Roundtable, this approach draws on several core principles.

Convexity

Allocating to positions with asymmetric payoff profiles, where the potential upside during stress scenarios exceeds the downside in calm markets. This may include long-volatility strategies, deep value opportunities with hard asset backing, and selective options overlays.

Diversification Across Regimes

Traditional portfolios assumed bonds would rally when equities sold off. That relationship broke down in 2022 and remains less reliable than many investors assume. True diversification means carrying exposures that can perform across multiple economic regimes — inflationary, deflationary, growth, and contraction environments.

Liquidity as a Strategic Asset

Liquidity is often underestimated in portfolio construction. Maintaining meaningful liquidity is not a drag on returns in volatile environments — it is a source of opportunity. Liquidity allows investors to deploy capital when dislocations are most severe, often when other market participants are forced sellers.

At Roundtable, portfolios are currently positioned with a tilt toward inflation-sensitive real assets, select quality equities with pricing power, liquid alternatives with low equity correlation, and tactical cash buffers sized for opportunistic deployment.

We are not abandoning equities — we are simply being more deliberate about which equities we own and under what conditions we increase exposure.

The Bigger Picture

Passive investing is not wrong. It is simply a strategy designed for a specific environment — one defined by coordinated central bank support, globalization, and steadily declining interest rates.

We are no longer clearly in that environment.

Managing capital as though those conditions still exist introduces risks that may not become visible until markets are under stress.

Active management in this context does not mean trading more frequently. It means thinking more deliberately about where risk is being taken, whether it is being compensated, and whether the portfolio structure improves or deteriorates when volatility increases.

The investors who compound wealth most effectively over the next decade will likely not be those who predicted every macro shift. They will be those whose portfolios were built to benefit from the uncertainty itself.